Not to blow my own trumpet… too much … in April last year, I was writing about how Australia was heading to a mortgage crisis. The issues that I saw unfolding were that politicians on both sides of the political fence had misplaced priorities regarding housing prices. Primarily, their focus was on getting more and more younger families into a market that looked and smelled like a bubble, while at the same time doing little to fix the long-term structural issues in the wider economy. As time has gone on, these initial thoughts have become more relevant.

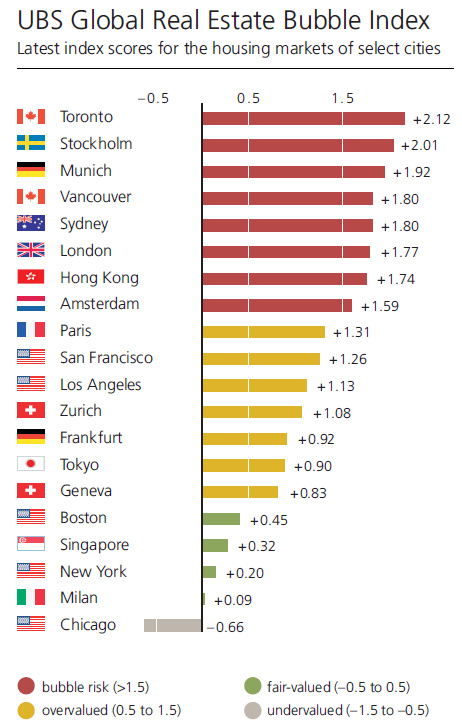

Across the major cities, year to date, the average housing prices have fallen by 0.8% and 1.4% in Sydney. The UBS Global Real Estate Bubble Index is “designed to track the risk of housing bubbles in global financial centres” Measuring such factors as price-to-income ratios, mortgage-to-GDP ratios and rental return to price, the UBS Global Real Estate Bubble Index currently lists 8 major cities as overvalued or at risk of being in a bubble.

With Sydney coming in 5th on that list, and the real prices for Sydney housing now shown to be declining, questions arise around the likelihood that we will we experience a pop as investors try to quickly sell off assets to mitigate the risk of loss.

Some reports indicate that more than 820,000 or 1 in 4 households are in some level of mortgage stress, which translates into 1 in 4 owner-occupied and 2 in 3 investment houses being on interest only loan repayments resulting in a total of $640 billion in interest-only loans outstanding. That number is so large that it roughly equates to 50% of the total Australian GDP.

UBS found that the average interest-only loan rate for owners occupiers went up nearly half-a-percentage point over the past year, while investors are paying about three-quarters of a percentage point more … The survey revealed that these rate rises have already left 71 per cent of recent interest-only borrowers under moderate to high levels of financial stress. – Michael Janda

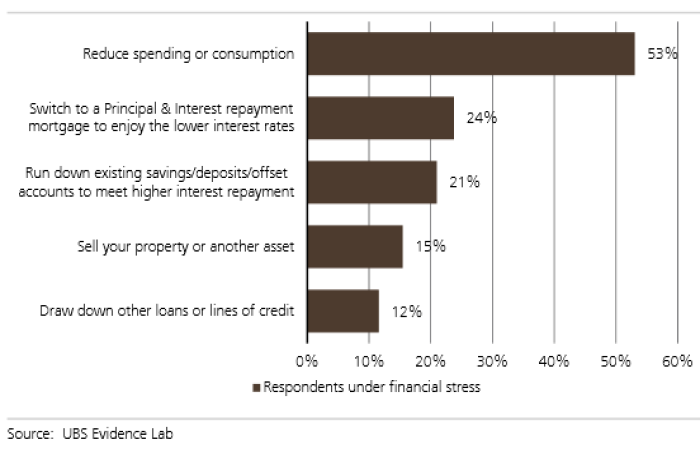

Based on the survey, more than half the respondents expected to cut back household spending with “a further 15 percent said they may sell their property or another asset, with nearly a quarter of those under high financial stress considering this option.

With this degree of at-risk mortgage leverage, the chances that we will see a gradual unwinding of housing prices and a smooth household de-leveraging, seem to be less and less likely. What is certain, the risk posed to the greater economy is huge.